JPMorgan Chase Embedded Payments

![]()

OVERVIEW

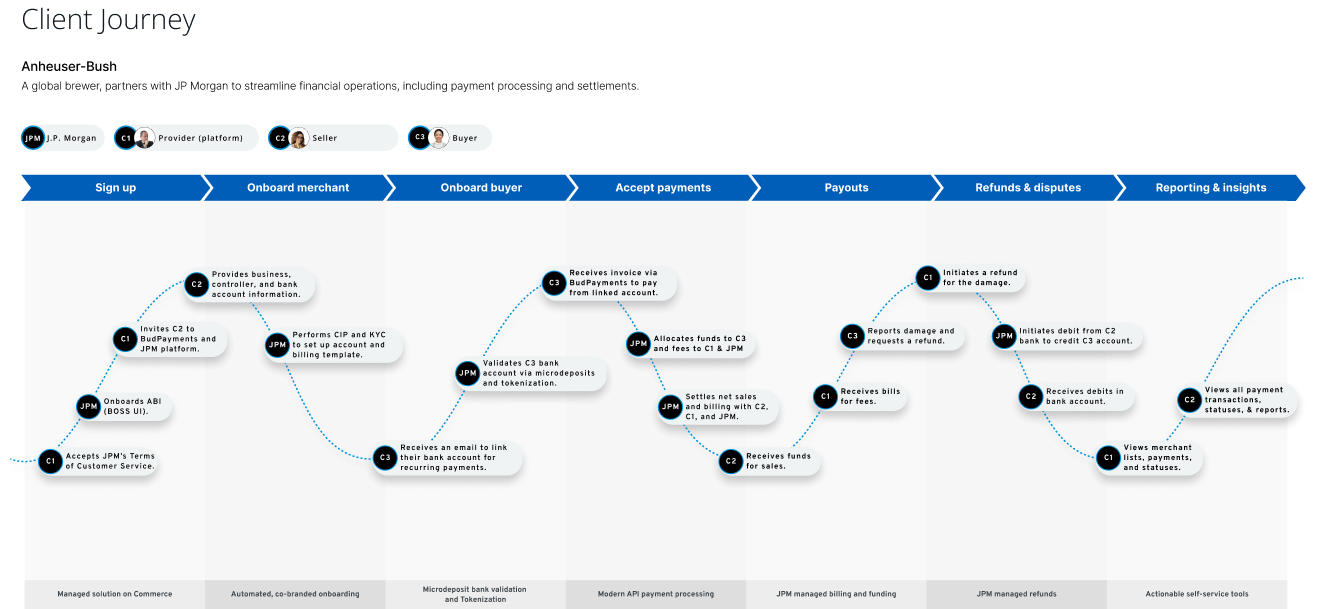

Problem: Enterprise platforms and growing businesses wanted to embed JPMorgan Chase payment capabilities into their products, but complex onboarding, payment flows, fees, permissions, ownership models, and servicing responsibilities made integration difficult to understand, configure, and scale with confidence.

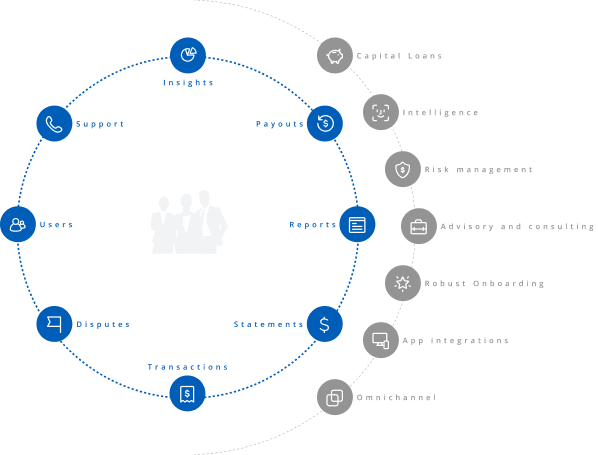

Solution: A modular embedded finance experience that simplified adoption through guided onboarding, configurable payment capabilities, transparent ownership and permission structures, and reusable workflows across pay-in, pay-out, PayFac, marketplace, and servicing experiences.

My Role & Impact: Directed the experience strategy and design direction across a six-month, zero-to-one delivery, translating research with seven enterprise clients into a modular product framework and aligning product, engineering, legal, risk, operations, research, and business teams around launch-critical decisions.

- Supported onboarding for 700+ early clients across the United States and Canada.

- Contributed approximately $1M in business value through reusable workflows and components.

- Reduced duplication across onboarding, configuration, permissions, ownership, and payment-capability workstreams.

- Established a scalable experience foundation for enterprise platforms, marketplaces, ISVs, and growing businesses.

- Guided parallel design workstreams from early definition through launch readiness within six months.

![]()

UX PROCESS

![]()

DISCOVERY

The discovery phase focused on understanding the embedded finance ecosystem from both the client and internal operating perspectives.

My team and I worked closely with product and research partners to understand how platform partners expected embedded solutions to work, what they needed to configure, where they experienced friction, and how they interpreted responsibilities across payments, onboarding, fees, ownership, and servicing.

Seven clients agreed to participate in interviews, which gave the team valuable insight into how embedded finance experiences needed to behave in real platform environments. These conversations helped us understand what clients expected from Chase, where they needed guidance, and what parts of the experience felt unclear or overly complex.

![]()

![]()

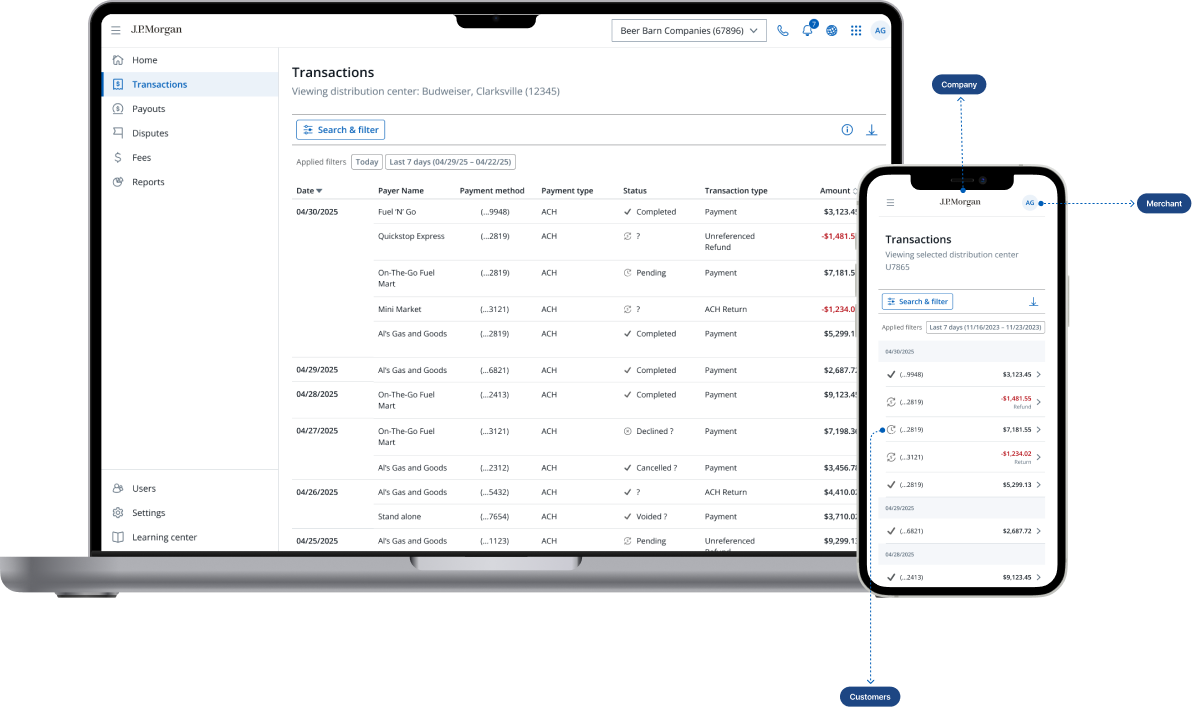

I also spent time learning the business and operational mechanics behind the product. This included delivery models, network charges, fee structures, pay-in and pay-out flows, PayFac models, marketplace relationships, pay-by-bank opportunities, and the different responsibilities between Chase, platforms, merchants, and end customers.

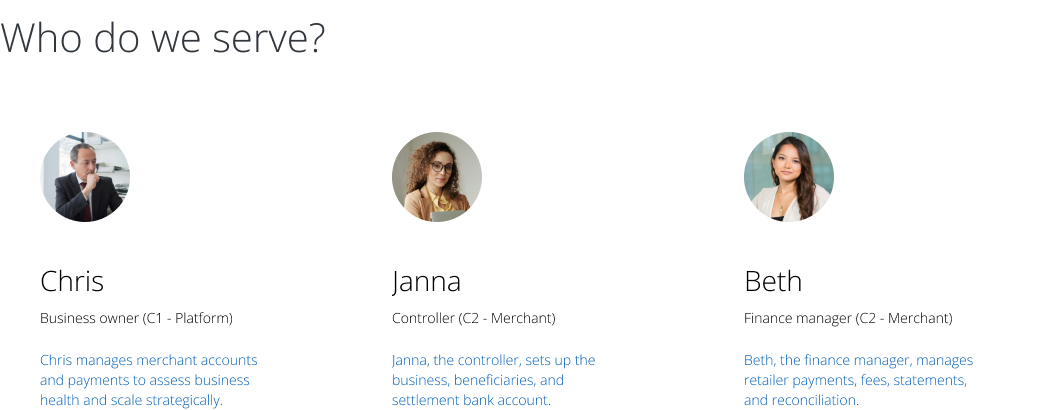

Discovery helped us identify the deeper issue: the experience needed to support several connected audiences at once. 100% of platform owners (C1) needed configuration and control. Merchants (C2) needed clarity and trust. End customers (C3) needed seamless payment experiences.

AI helped accelerate portions of this phase by organizing research themes, summarizing workshop input, and making insights easier to socialize. This improved speed and communication, but design judgment remained central. Every concept still required human review, product reasoning, and financial context.

![]()

DEFINE

The goal was to move from broad complexity into a clear product structure. We needed to define who the experience served, what each user group needed, which workflows were universal, which workflows needed configuration, and where reusable components could reduce duplication.

I defined primary audiences across the ecosystem: platform users, merchants, business owners, Chase internal teams, and downstream customers. We mapped their responsibilities, needs, and decision points so the team could understand how each group interacted with the embedded finance experience.

A major shift happened during this phase. The work moved from a set of complex payment requirements into a modular experience framework.

![]()

![]()

IDEATE

My team and I explored how embedded finance capabilities could be presented in a way that felt clear, flexible, and scalable. We needed to support sophisticated enterprise platforms while also creating patterns that could eventually serve smaller businesses with less financial infrastructure knowledge.

I designed concepts across multiple workstreams, including onboarding, platform setup, merchant setup, pay-in, pay-out, PayFac, marketplaces, pay-by-bank, ownership, permissions, configuration, and internal servicing integrations at scale.

![]()

![]()

Rather than treating each workflow as a separate experience, I guided the team to design around scalable modules and adaptive navigation patterns. The modular approach reduced one-off design decisions and created a more flexible experience foundation that could scale across enterprise platforms, marketplaces, ISVs, and growing businesses without reinventing the product each time.

Cross-functional workshops became a key part of ideation. These sessions helped teams evaluate concepts together, discuss constraints, identify risks, and align on what was feasible and valuable. They also created space for product, engineering, business, legal, risk, and operations partners to contribute earlier in the process, which reduced downstream rework.

Throughout ideation, I kept the team focused on practical outcomes. The goal was not to generate more design options for the sake of exploration. The goal was to create the right patterns: patterns that simplified the experience, supported delivery, and could scale across future embedded finance opportunities

![]()

![]()

TEST

My ux team and I used prototypes, stakeholder reviews, research insights, design critiques, and cross-functional working sessions to evaluate whether the experience direction was clear, usable, feasible, and aligned with business goals.

I reviewed whether onboarding steps made sense to clients, whether configuration flows reduced confusion, whether payment capability groupings were logical, and whether ownership responsibilities were clear. I also tested whether the modular patterns could support different client types and business models without creating unnecessary complexity.

Validation helped us identify gaps early. Some areas needed clearer language. Some workflows needed stronger guidance. Some configuration patterns needed to better reflect how platforms and merchants understood their responsibilities. Some assumptions needed to be checked against legal, risk, operational, or engineering constraints.

This phase also helped build trust across stakeholders. Product leaders could see how design decisions connected to client needs and business goals. Engineering teams could evaluate feasibility earlier. Business and operations teams could see how the experience supported scale. Risk and legal partners could help ensure the product direction respected financial service requirements.

Testing was not treated as a final checkpoint. It was used as an alignment mechanism throughout the work.

![]()

![]()

![]()

EXECUTE

This was where the work became sharper, more consistent, and more delivery-ready. My team and I refined workflows, improved information architecture, aligned patterns with the design system, clarified interaction details, and strengthened the final storytelling around the experience.

This phase required strong coordination because several workstreams were moving at the same time. I helped keep designers focused, connected cross-functional partners to the right decisions, and ensured the work stayed aligned to launch priorities.

I prioritized the team maintain momentum. In fast-moving product environments, leadership is not only about setting direction. It is also about protecting focus, creating confidence, and helping people move through ambiguity without losing energy.

By the end of this phase, the work was structured, scalable, and connected to a broader business strategy.

![]()

![]()

IMPACT

The initiative delivered meaningful value across product delivery, business alignment, client readiness, and design scalability.

Within six months, I empowered the team to deliver a zero-to-one embedded finance experience that supported expansion across the United States and Canada and enabled onboarding for 700+ early clients.

Together, we introduced a modular design approach that created reusable workflows and components, contributing approximately $1M in business value. This helped reduce duplicated effort across workstreams by giving teams clearer patterns for onboarding, configuration, ownership, and payment capability setup.

![]()

![]()

I helped strengthen alignment between JPMorgan Chase’s embedded finance priorities and Chase small business opportunities by keeping the work grounded in reuse, scalability, and client needs. This created a foundation that could support sophisticated enterprise platforms while preparing the experience for broader adoption among small and medium businesses.

![]()